From OMS to OEMS: Why banks need a modern execution operating model for retail trading

Retail trading has changed. For banks and securities institutions, the challenge is no longer limited to receiving, managing, and routing orders. The modern execution environment now requires high-volume order handling, low-latency processing, Smart Order Routing, Best Execution policy control, RFQ workflows, internalization, proprietary pricing, hedging, and seamless integration with downstream systems.

This shift is forcing many institutions to reassess whether a traditional Order Management System, or OMS, is still enough.

For banks managing retail order flow, the next stage is not simply an OMS upgrade. It is the move toward a modern Order and Execution Management System, or OEMS: a central execution hub that connects order capture, routing, pricing, execution, internal liquidity, hedging, market data, and post-trade processes in one controlled operating model.

What is an OEMS?

An Order and Execution Management System is a trading technology platform that combines order management and execution management capabilities.

A traditional OMS is primarily designed to capture, manage, and track orders. A modern OEMS goes further. It supports the full execution lifecycle, including order routing, execution algorithms, broker and venue connectivity, Best Execution policy configuration, RFQ workflows, internalization, and integration with risk, position keeping, reporting, and back-office systems.

For banks and securities institutions, this distinction matters. Retail execution is becoming more complex, more automated, and more strategically important. Institutions need platforms that can support scale, control, adaptability, and execution quality at the same time.

Horizon’s OEMS solution is single integrated platform covering order routing and execution, advanced execution strategies such as Smart Order Routing and algorithms, quoting and hedging workflows, order internalization, and multi-asset trading capabilities across cash equities, derivatives, structured products, fixed income, digital assets, and more…

Why traditional OMS architecture is no longer enough

A traditional OMS can be effective for basic order capture and order management. However, retail trading environments now require much more.

Banks are facing growing demands across several dimensions:

- higher volumes of retail order flow;

- demand for faster and more resilient execution;

- more sophisticated Best Execution obligations;

- the need to connect to multiple venues, brokers, and internal liquidity sources;

- growing interest in RFQ and direct trading workflows;

- pressure to internalize eligible flow where appropriate;

- support for 24/7 trading;

- the need to integrate execution with risk, positions, reporting, and back-office systems;

- demand for proprietary pricing, routing, and hedging logic.

The result is a more complex execution environment. A bank may need to collect client orders from digital channels, determine the correct execution path, apply configurable Best Execution policies, access external venues or brokers, evaluate internal liquidity, manage RFQ workflows, distribute prices, execute or hedge the resulting position, and provide downstream information to internal systems.

This cannot be treated as a set of disconnected components. It requires a central execution layer.

The rise of the execution hub

A modern OEMS acts as an execution hub for the institution.

Instead of separating order capture, routing, execution, pricing, hedging, and integration into fragmented systems, the OEMS provides a controlled environment where these functions work together.

For banks, this creates several advantages.

First, it improves operational control. Teams can manage execution logic, routing policies, workflows, and connectivity in a more coherent architecture.

Second, it supports scalability. High-volume retail order flow requires low latency, resilience, and robust processing capacity.

Third, it enables better execution governance. Best Execution policies can be configured into the routing and execution workflow rather than reviewed only after the trade.

Fourth, it supports strategic evolution. Banks can progressively add direct trading, RFQ, internalization, proprietary pricing, auto-hedging, and additional asset classes without redesigning the entire architecture.

Horizon positions its platform as a central execution hub capable of supporting order collection, Smart Order Routing, Best Execution policies, Direct Trading workflows, RFQ lifecycle management, proprietary quoting algorithms, internal marketplace capabilities, auto-hedging, and execution across venues and brokers.

Best Execution must be built into the workflow

Best Execution is often discussed as a regulatory or reporting topic. But for banks handling retail order flow, it should also be understood as an execution design topic.

A modern OEMS should help institutions configure and apply Best Execution logic directly inside the workflow. This includes rules and policies for venue selection, broker routing, internal liquidity evaluation, order handling, execution algorithms, and directed order flows.

The key question is not only whether the institution can demonstrate what happened after execution. It is whether the institution can control how execution decisions are made before and during the order lifecycle.

That requires configurable policies, clear auditability, integration with market data and execution venues, and the ability to adapt routing logic as market structure, regulation, and business priorities evolve.

Smart Order Routing as a strategic capability

Smart Order Routing, or SOR, is central to the modern OEMS operating model.

In a retail execution context, SOR helps determine where and how an order should be executed, considering factors such as price, liquidity, venue availability, execution probability, cost, speed, and the institution’s own execution policy.

For banks, SOR should not be viewed as a standalone module. It should work together with order management, market data, broker connectivity, execution algorithms, internal liquidity, Best Execution policy, and reporting.

When properly integrated, Smart Order Routing allows banks to create a more dynamic and controlled execution model.

RFQ and direct trading workflows are becoming more important

Retail execution is also evolving beyond simple order routing.

Many banks are exploring or expanding RFQ and direct trading workflows. In these models, the institution may need to receive a client request, generate or source a price, manage the RFQ lifecycle, distribute prices in real time, execute the trade, and hedge the resulting risk.

This requires more than connectivity. It requires orchestration.

A modern OEMS should support the full RFQ lifecycle, including request capture, pricing, quote distribution, trade execution, controls, and downstream integration. Where proprietary pricing logic is part of the institution’s differentiation, the OEMS should also allow that logic to be integrated without forcing the bank into a closed operating model.

Internalization: from execution choice to operating model

Order internalization is becoming a strategic topic for banks with significant retail flow.

Internalization can help institutions improve execution control, access internal liquidity, reduce external execution dependency, and create new liquidity provision models. However, internalization must be handled carefully. It requires robust pricing, risk controls, hedging, Best Execution governance, and operational transparency.

In other words, internalization is not just a trading decision. It is an operating model.

An OEMS that supports internal marketplace capabilities, proprietary pricing, quoting, RFQ workflows, and auto-hedging can help banks progressively develop internalization while maintaining the controls required in a regulated environment.

Why extensibility matters

No two banks have exactly the same execution model.

Each institution has its own architecture, channels, trading workflows, asset classes, regulatory constraints, proprietary logic, and strategic roadmap. This is why extensibility is one of the most important characteristics of a modern OEMS.

An extensible platform allows a bank to integrate with existing systems, implement proprietary pricing logic, adapt routing policies, manage RFQ workflows, define hedging strategies, and evolve as business requirements change.

This is especially important for institutions that want to preserve differentiation. A bank should not have to choose between using a vendor platform and maintaining ownership of its proprietary execution logic.

The strongest OEMS platforms combine standard trading functionality with flexible extension capabilities.

In Horizon’s, the Horizon Extend© framework is positioned as a way to integrate with the existing IT landscape, implement proprietary logic such as pricing, routing policies, RFQ handling, and hedging strategies, and adapt to new business or regulatory requirements.

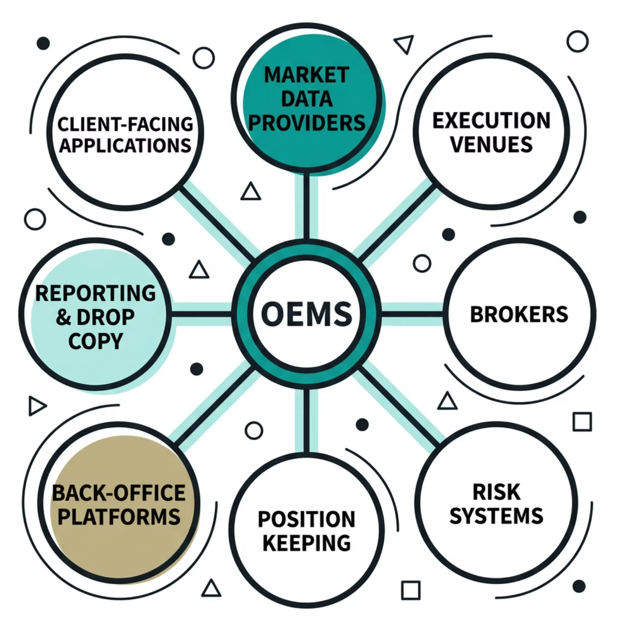

Integration with the banking ecosystem

A modern OEMS cannot operate in isolation.

It needs to connect with the institution’s broader trading and banking ecosystem, including:

- client-facing applications;

- market data providers;

- execution venues;

- brokers;

- risk systems;

- position keeping systems;

- back-office platforms;

- reporting tools;

- drop copy flows;

- market connectivity infrastructure.

Integration is therefore a key selection criterion. A platform may perform well in a demonstration, but the real test is whether it can operate reliably inside a complex banking environment.

Banks should evaluate not only functionality, but also implementation approach, professional services capability, flexibility, deployment model, support structure, and the vendor’s experience with complex financial institutions.

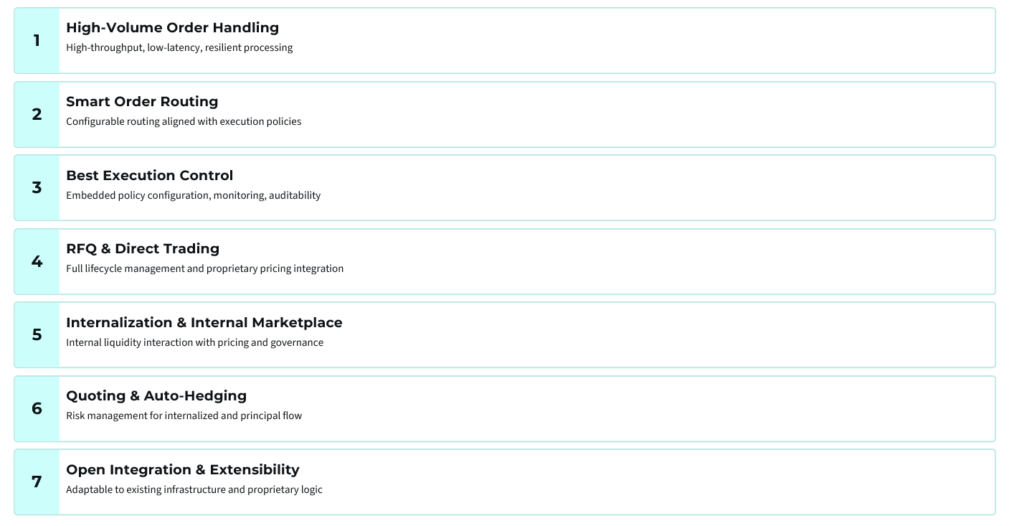

What capabilities should banks look for in a modern OEMS?

When evaluating an OEMS platform, banks and securities institutions should look for capabilities across seven areas.

1. High-volume order handling

The platform should support high-throughput, low-latency, resilient processing for retail order flow.

2. Smart Order Routing

The OEMS should support configurable routing logic aligned with the institution’s execution policies.

3. Best Execution control

Best Execution should be embedded into the workflow, with clear policy configuration, monitoring, and auditability.

4. RFQ and direct trading

The platform should support RFQ lifecycle management, price distribution, direct trading workflows, and integration with proprietary pricing.

5. Internalization and internal marketplace

The OEMS should enable eligible order flow to interact with internal liquidity where appropriate, supported by pricing, controls, and governance.

6. Quoting and hedging

The platform should support quoting workflows and auto-hedging mechanisms to manage risk from internalized or principal flow.

7. Open integration and extensibility

The system should integrate with existing infrastructure and allow the institution to adapt proprietary logic over time.

The partner question: technology is only part of the decision

Selecting a modern OEMS is not only a technology decision. It is a strategic operating model decision.

Banks should ask:

- Can the partner support high-volume execution environments?

- Can the platform evolve as the bank’s trading model evolves?

- Can proprietary logic be integrated without creating unnecessary dependency?

- Can the vendor work effectively with trading, technology, risk, operations, and compliance teams?

- Can the solution be deployed in a way that reduces implementation risk?

- Can the platform support both current requirements and future execution models?

The right partner should bring both platform capability and practical implementation expertise.

For banks moving from traditional order management toward a modern execution hub, this combination is essential.

Conclusion: the future of retail execution is integrated, configurable, and controlled

Retail execution is entering a new phase.

Banks and securities institutions need to manage higher volumes, more complex routing decisions, Best Execution expectations, RFQ and direct trading workflows, internalization opportunities, and tighter integration across the trading lifecycle.

A traditional OMS was not designed to carry all of this alone.

A modern OEMS gives institutions a path toward a more scalable, controlled, and future-ready execution operating model. It connects order management, execution management, routing, pricing, RFQ, internalization, hedging, and integration into one architecture.

For banks, the opportunity is clear: move from managing orders to controlling execution.

Frequently Asked Questions

A traditional OMS is primarily designed to capture, manage, and track orders, while an OEMS (Order and Execution Management System) goes further by supporting the full execution lifecycle. This includes order routing, execution algorithms, Smart Order Routing, Best Execution policy configuration, RFQ workflows, internalization, and integration with risk, reporting, and back-office systems in a single platform.

Modern retail trading environments demand high-volume order handling, low-latency processing, multi-venue connectivity, sophisticated Best Execution compliance, RFQ workflows, internalization, and proprietary pricing logic. These complex requirements cannot be effectively managed by disconnected components, necessitating a central execution hub that a traditional OMS architecture simply cannot provide.

Smart Order Routing (SOR) within a modern OEMS determines where and how an order should be executed by evaluating factors such as price, liquidity, venue availability, execution probability, cost, and speed. It works in conjunction with order management, market data, broker connectivity, execution algorithms, internal liquidity, and Best Execution policies to create a dynamic and controlled execution model.

Best Execution should be built directly into the execution workflow rather than treated solely as a post-trade reporting obligation. A modern OEMS enables institutions to configure and apply Best Execution logic through rules and policies for venue selection, broker routing, internal liquidity evaluation, and execution algorithms — ensuring execution decisions are controlled before and during the order lifecycle.

Order internalization allows banks with significant retail flow to execute orders against internal liquidity rather than routing them to external venues, improving execution control and reducing external dependency. However, it requires a full operating model approach with robust pricing, risk controls, hedging, Best Execution governance, and operational transparency — capabilities that a modern OEMS with internal marketplace and auto-hedging features can support.