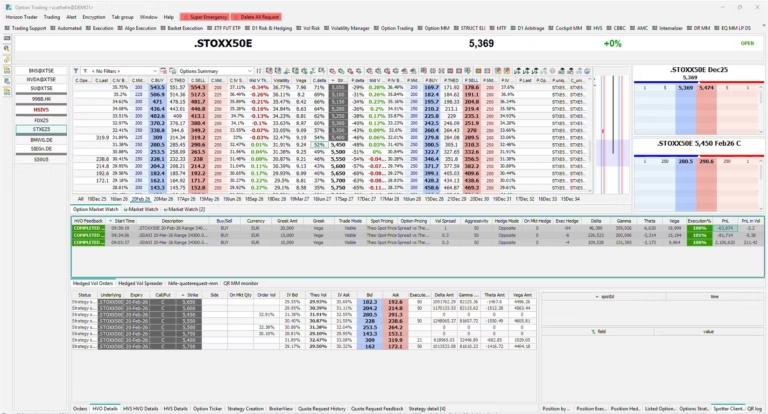

This algo automates the execution of option trades in order to buy or sell a given amount of greeks (vega, gamma or theta).

An HVO can be executed on a single strike or a range of strikes. It minimizes market impact by splitting the amount for each order into buckets, determined by the strategy’s parameters. The delta risk incurred by the option’s trades is automatically hedged.

Hedged Vol Spreader (HVS)

This algo leverages HVO functionalities to build a spread position between the volatility of various underlying stocks, indices, and other instruments – buying some and selling others. It can be used to execute dispersion trades.

Volatility Automatic Fitting

This algo automatically fits the volatility curves using Horizon models. The algo can be triggered at regular intervals, on a spot move or on user action.

Discover Horizon's Volatility trading now:

Watch the webinar replay from January 29, 2026 – Move from manual delta-hedging to scalable, systematic volatility execution.

Managing Gamma and Vega: Practical and Customizable Frameworks for Volatility Trading

Agenda:

The Scalability Constraint: Analyzing how manual position management limits bandwidth and consistency for specialized desks (Delta One, Options, Algos).

Design-Led Exposure: Moving from trading instruments to trading Exposure Profiles, concentrating risk in volatility rather than direction.

The HVO/HVS Framework: A deep dive into Hedged Volatility Orders and Spreads to automate the “heavy lifting” of delta neutrality.

Portfolio-Level Management: Extending the framework to baskets, index components, and correlated assets.

Live Implementation Demo: A technical walkthrough of structuring, hedging, and scaling volatility positions in real-time.

Subscribe to Horizon 's Newsletter!

Subscribe to our newsletter and stay updated on our latest news!

Request a Demo !

Please provide your details and your demo request and we will get back to you.

Fill this Form to Download our Brochure

Upon entering the requested information, you will receive a link that will redirect you to a page where you can download our Brochure.